Recently, my partner in investment strategy, Byron Wien, reminded me that pessimists generally do not survive long in finance. Byron entered the finance world nearly 60 years ago. At 89 years young today, his relentless curiosity, creativity and insights continue to inspire and are a testament to the power of optimism.

I’ve been thinking about this valuable lesson as headlines in the financial press and investor sentiment turn increasingly sour. This sentiment is easy to understand, with the S&P 500 officially entering a bear market and many equity markets around the world in similar straits. Combine that with historically poor performance in traditional fixed income, and the result is the worst YTD performance for the 60/40 portfolio since the 1960s. [ 1 ] The economy and markets face important near-term challenges, including unrelenting inflation and coordinated central bank tightening that will most likely lead to a recession at some point.

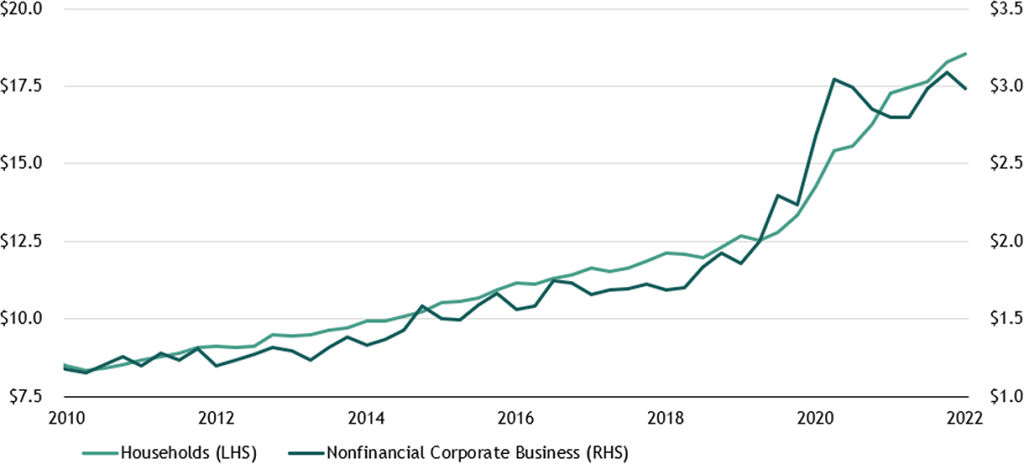

And so, these days, virtually every conversation I have includes this question: “When?” I’ve consistently taken the “over” on the consensus view of a recession because of the still-strong cushion of household excess savings and the high level of cash on corporate balance sheets. These two factors are primary reasons why there is still strength in the economy.

Focusing too intently on when a recession might strike carries risk. During challenging conditions, people seem to forget that economic cycles are just that—cyclical. And that cycles have their ups and their downs. In the end, healthy economies grow, and markets generally move up and to the right over long periods. If greed were investors’ worst enemy at the top of a market, fear is their worst enemy when markets are challenged. The winner in either environment will be the clear-eyed investor who considers the long-term fundamentals and invests with conviction in themes that can deliver attractive risk-adjusted returns.

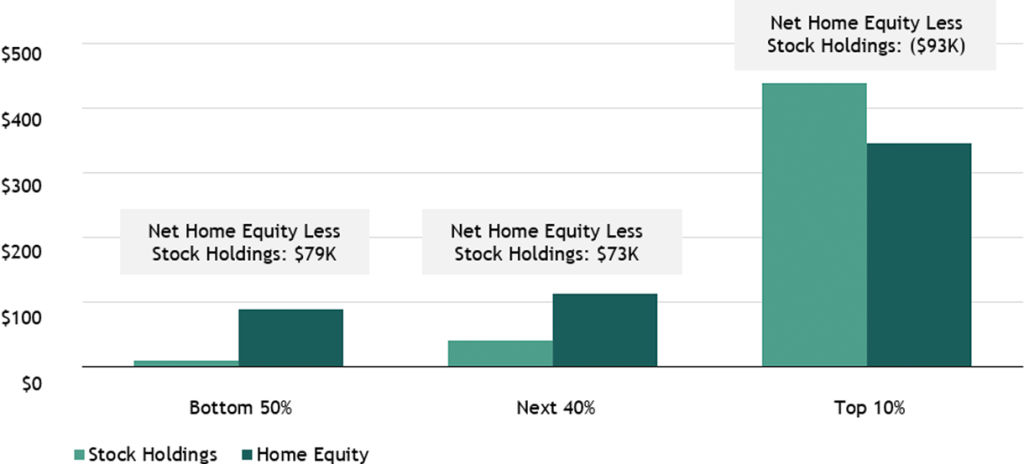

In this month’s essay My team and I evaluate recession indicators while considering near-term macroeconomic headwinds. Also, to gauge the timing and depth of a potential recession, we look at how today’s fundamentals compare to historical examples. We draw out key differences between these examples and highlight that the recovery looks significantly different in each instance based on two key factors: labor markets and housing. On US housing, which we view as critical to understanding the potential severity of this next recession, we remain optimistic about its secular prospects.

Market Views

One-on-One with Michael Zawadzki: The Long and Growing Runway for Private Credit

December 06, 2024