A growing number of infrastructure projects – from data centers to EV charging stations – are waiting to be connected to the US power grid.

In fact, it is estimated that these new projects will require twice the country’s current power generation capacity.

It will cost an estimated ~$3.9 trillion – the equivalent of $1.5 billion for every gigawatt of power – to fill this infrastructure gap.1

We believe that this demand will help boost economic growth and create near-term and long-term jobs.

US Power Grid Transmission Queue

Source: Lawrence Berkeley National Laboratory, as of April 2024.

S&P as of July 2024, and LevelTen Energy Report as of June 2024. This figure is based on the fact that over 90% of the interconnection queue is renewables (wind and solar) and amount to $1.5Bn/GW to build in North America.

History suggests lower rates support both private equity buyers and credit lenders as M&A activity increases.

In North America, there is $1.5 trillion of dry powder in private equity, now being put to work as the Fed lowered rates.1

Private credit is financing these transactions, filling the gaps left by traditional bank lenders.

The shift is structural—private lenders accounted for 86% of all leveraged buyouts in 2024 versus 65% in 2021.2

M&A Deal Volume

($ in billions, from 1985-2023)

Sources: Federal Reserve, Capital IQ and Thomson Reuters, as of December 31, 2023. M&A deal volume covers annual data from 1985-2023. Higher and lower rate environments determined by the annual 10-year US Treasury yield and whether it is above or below the average 10-year yield over the full period (1985-2023).

Preqin, as of June 30, 2024. Reflects latest data available and North America dry powder.

Pitchbook LCD, as of June 30, 2024, and December 31, 2021.

Investors generally remain focused on a small number of mega-cap companies.

But for private equity investors, the opportunity exists in public mid-size companies, which are trading at the most attractive valuations in over 20 years.

Blackstone recently acquired mid-size companies in digital media and software/technology at a significant discount to their publicly traded peers.

We are watching mid-size businesses with strong fundamentals that others might overlook.

Public-to-Private Transactions

Source: Blackstone, S&P Capital IQ as of 6/30/2024. BX completed deal represents each respective Blackstone completed deal TEV at cost/NTM EBITDA. Median public company represents TEV/NTM EBITDA for comparable public peers from S&P Capital IQ and represents latest Blackstone analysis.

E-commerce growth has been a powerful tailwind for logistics real estate.

Consumer expectations for faster delivery are pushing e-commerce retailers to compete for faster shipping times – Amazon’s average delivery turnaround has decreased to 1.5 days vs. 4.1 days in 2020.1

Meeting today’s consumer demands requires strategically located warehouses in densely populated areas.

Where you invest matters: Blackstone is a global leader in last-mile logistics investing.

Growth in Sales and Deliveries

(Percent Year-Over-Year, FY 2023)

Source: Brick and Mortar and E-Commerce Sales: U.S. Census Bureau, as of December 31, 2023. Brick and mortar sales reflect total retail sales excluding motor vehicles and parts dealers, gasoline stations, food services and e-commerce sales. Amazon: Amazon 2023 Letter to Shareholders, as of April 11, 2024.

NielsenIQ, as of September 18, 2023. Reflects the number of days from an online purchase transaction to package arrival from Q2 2020 to Q2 2023.

According to TSA data, the US has seen 12 of the 15 busiest travel days on record since mid-May.1

International-bound travel is particularly strong. As of May, over 28 million Americans have traveled abroad in 2024 – the most in this time period over the past five years.2

At Blackstone, we recognized the “revenge travel” trend early, which helped inform investments across our real estate and private equity businesses.

Daily Volume of Travelers Screened by TSA

(7-day Moving Average, Millions of Passengers)

Source: Transportation Security Administration and Macrobond, as of July 9, 2024.

Transportation Security Administration, as of July 9, 2024.

International Trade Association, as of May 31, 2024.

If you look at the real estate cycle coming out of the GFC, values bottomed well before market sentiment suggests.

While headlines remained negative for years, values were actually improving.

We are focused on the long view, not the rear view – deploying capital in an opportunity-rich environment, much like today.

Commercial Real Estate Values Through the GFC1

Indexed, June 2007 = 100

Note: Represents Blackstone’s view of the current market environment as of the date appearing in this material only. There can be no assurance that the trends described herein will continue or not reverse.

Green Street Advisors, as of December 31, 2023. Reflects the Commercial Property Price Index, which captures the prices at which US commercial real estate transactions are currently being negotiated and contracted. Equally weights Core Sectors: multifamily, office, industrial and retail.

Reuters, as of July 29, 2009. Wall Street Journal, as of August 25, 2010. Forbes, as of October 3, 2012.

Commercial mortgage-backed securities (CMBS) issuance has picked up meaningfully, up nearly 5x in Q1 2024 vs Q1 2023.

CMBS spreads have narrowed, bringing down the cost of capital.1

More accessible commercial real estate debt is likely to drive greater transaction activity.

US CMBS Issuance Activity

($ in billions)

Source: Green Street Advisors, as of March 31, 2024. Issuance data is for single asset single borrower CMBS loans.

Blackstone proprietary data, as of March 31, 2024. CMBS spreads denoted as high quality (AAA) spreads across multi-family, industrial, data centers and manufactured housing sectors.

The US has had a rapid increase in trade with Mexico, Vietnam, Central/South America and Europe over the past few years.

These changing trade patterns have driven east and gulf coast ports to have some of the fastest growth in shipping volumes.1

This has contributed to $222B in US manufacturing construction in February 2024 – over 2x 2021.2

We are seeing this in real time through our port and logistics businesses.

Shifting US Trade Patterns

($ in billions)

Source: US Census Bureau, as of December 31, 2023. Data is annual total trade in goods.

Based on Moffatt & Nichol and Ports Authority data as of May 2023. Comparison based on 2017-2022 actual volume growth CAGRs.

US Census Bureau, as of April 1, 2024. Manufacturing construction spending represents monthly value of construction put in place (seasonally adjusted annual rate) in real US dollar terms.

The transition to a digital world and the explosion of AI are driving a need for data centers worldwide.

India has only 52% internet penetration among its citizens (versus 92% in the US). This, coupled with a low cost of data, has led to an exponential increase in data consumption.1

Despite rapidly growing tech adoption, India’s data center capacity is still a fraction of leading global markets.

Data center stock comparison

(MW / million population)

Source: datacenterHawk, JLL (1H 2023 Datacenter Outlook), Structure Research, World Bank. MW / million population is computed based on national population estimates. Data is based on third party operators and does not include self-build data centers by firms.

Internet in India Report (2022), DataReportal Digital Report (2022), cable.co.uk (2023), Nokia Mobile Broadband Index (2023)

Represents Frankfurt, London, Amsterdam and Paris which are primary data center hubs in Europe. Population for FLAP is represented by Germany, Netherlands, France and United Kingdom.

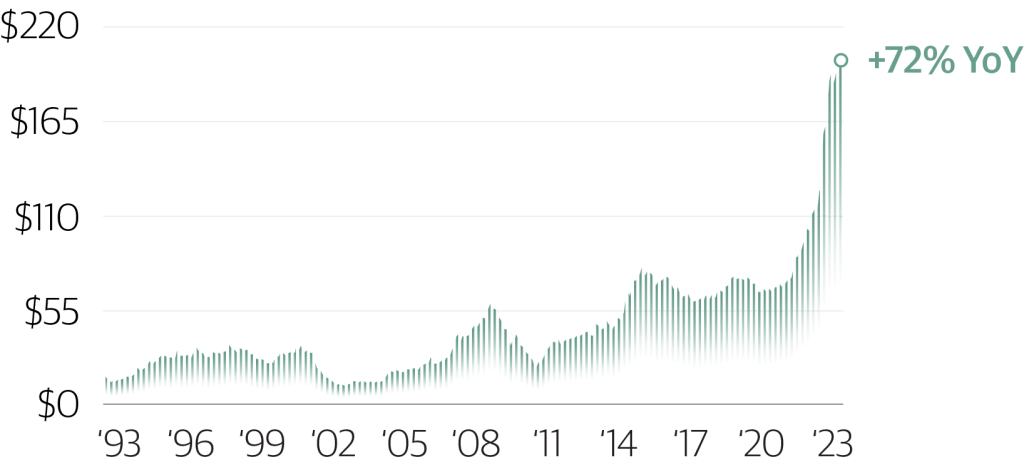

US private manufacturing construction is up 72% from a year ago, with 71% currently focused in the south and west.1

Every durable manufacturing job creates nearly 9 related jobs—a tailwind for these regions, which are already experiencing strong growth in population, jobs and wages.2

More broadly, $110 billion in new clean energy investments have been announced due to recent government incentive programs, with an additional $910 billion for manufacturing and infrastructure projects.3

We see these trends continuing to benefit demand for investments in the energy transition, as well as commodities, logistics, storage and transportation.

Total US Private Manufacturing Construction Spending

($ in billions; seasonally adjusted annualized rate)

Source: US Census Bureau, as of 10/31/2023.

US Census Bureau, as of 10/31/2023. Data reflects value of private construction put in place for manufacturing.

Economic Policy Institute, as of 1/23/2019.

https://www.whitehouse.gov/invest/. Data reflects announcements since the IRA, CHIPS Act, and IIJA were enacted ($36 billion in announced investments and $74 billion in commitments for clean energy projects, and $356 billion in announced investments and $554 billion in commitments for manufacturing and infrastructure projects).

Larger companies are often well-positioned for elevated rates and growth challenges.

Companies with EBITDA of under $50 million have historically defaulted at more than five times the rate of companies with EBITDA of over $100 million.1

We believe lending to larger companies is one important way for private credit managers to protect capital today.

By Joe Zidle and the Portfolio Operations Procurement Team

If this is the final round of the inflation fight, it feels like the longest, with US producer prices up 2.2% year-on-year in September, the third consecutive monthly increase.1

Yet survey data from a subset of Blackstone portfolio companies suggests a more encouraging shift.

Nearly Flat Input Costs: In Q3, companies responding to our survey of Chief Procurement Officers reported just a 0.2% year-on-year increase in the average cost of manufacturing products or delivering services, a significant deceleration from 4.9% in Q4 of 2022.2

Sector-Specific Relief: Industrial & Services sector companies reported a 2.3% decline in their input costs, the first indication of disinflationary forces at play within these companies.

Surveyed Companies’ Reported Input Costs (YoY%)

US Bureau of Labor Statistics, as of 9/30/2023.

The Blackstone 3Q’23 survey of a subset of portfolio company CPOs referred to herein reflects input from 100 Blackstone portfolio companies (138 individual responses), largely within Blackstone’s Private Equity and Real Estate businesses (the “CPO Survey”). The 2Q’23, 1Q’23 and 4Q’22 CPO surveys reflect input from 107 portfolio companies (148 individual responses), 102 portfolio companies (131 individual responses) and 67 portfolio companies (59 individual responses), respectively. Certain portfolio companies have multiple procurement representatives and accordingly provided multiple responses per company to survey questions. Procurement representative responses from a single company in a single region are averaged when results are aggregated. Quarter-over-quarter presentations may reflect responses from different companies. The responding portfolio companies are not necessarily a representative sample of companies across Blackstone’s portfolio. The views expressed by responding portfolio companies do not necessarily reflect the views of Blackstone. Input costs include direct and indirect cost of operations including components, goods, services, energy, and G&A, and excluding human capital, wages, and benefits.

Canada’s population is booming, with the fastest annual growth in over six decades.1

Growth is driven by the country’s pro-immigration policy; ~60% of new immigrants hold a bachelor’s degree or higher.2

Rental housing and logistics supply has not kept up with increased demand, driving low vacancies of <2%.3

G7 annual population growth

Government sources and Macrobond, as of 1/31/2023 (US, as of 12/31/2022 and UK, as of 12/31/2021). Population growth rate calculated as percentage change from prior year.

Note: The EU average is based on population data for France, Germany and Italy, weighted by each country’s share of the combined total.

StatCan, as of November 2022. Represents percentage of total immigrants aged 25 to 64 with a bachelor’s degree or higher from 2016-2021.

Canada Mortgage and Housing Corporation, as of December 31, 2022 and CBRE, as of June 30, 2023. Housing figures reflect average vacancy for two-bedroom apartment units. Logistics figures reflect stock-weighted averages across Toronto, Montreal and Vancouver.

India’s GDP has grown 75% over the last decade and its equity market has returned more than 2.5x, outperforming most major global indices.

Shifting supply chains have also led to surging foreign direct investment in Indian manufacturing—up 76% year-on-year through 2022.

With the world’s largest population, a fast-growing middle class and an expanding manufacturing base, India is poised to continue outperforming.

10-year total return by equity market

(USD; indexed to 100 as of October 2013)

Macro indicators from United Nations and World Bank. FDI growth from S&P Global. Equity performance from Bloomberg, Macrobond, MSCI Inc., Standard & Poor’s and Stoxx as of September 12, 2023.

August 14, 2023

Encouraging Signs in Fed’s Inflation Fight

US inflation is cooling rapidly.

In fact, 90% of July CPI is attributed to the 7.7% yoy increase in reported shelter costs.

But what Blackstone recognizes through its extensive real estate holdings is that the government data lags the market.

Strip out that lagging shelter data and the extent of headline and core CPI inflation deceleration becomes much clearer…

US headline and core CPI, ex-shelter (% yoy)

US Bureau of Labor Statistics, and Macrobond, as of July 31, 2023.

July 31, 2023

Explosive Growth in Data

Cloud computing, content creation and the AI revolution are driving rapid growth in data.

Between 2010 and 2022, data created, consumed and stored increased 49x.1

This is fueling demand for US data centers, with more leasing in the last 18 months than in the previous six years combined.2

Global data created, consumed and stored (zettabytes)

IDC, as of December 31, 2021. 2021 and 2022 represent year-end estimates.

datacenterHawk, as of December 31, 2022. Demand based on total gross absorption in megawatts (electricity consumption).

July 24, 2023

Not All Real Estate Is Created Equal

Concerns about commercial real estate overlook dramatic dispersion across subsectors.

US public data center REITs are up 19.4% year-to-date, given accelerated fundamentals, with apartments and logistics also up strongly.1

Conversely, US office is seeing all-time high national availability of 26%,2 reflected in office REITs down 16.2% year-to-date.

US Public REIT performance year-to-date

FTSE NAREIT, as of June 30, 2023. Reflects total return of publicly traded REITs by NAREIT subsector from December 30, 2022, to June 30, 2023.

CoStar, as of March 31, 2023. Based on Class A buildings greater than 100,000 sf, excluding owner-occupied buildings.

July 17, 2023

An Attractive Environment for Private Credit

Higher base rates and wider spreads have been generating higher yields in non-investment grade private credit.

Returns have increased from 7.2% to 12.5% since 2021.

Yields for non-investment grade direct loans

Blackstone Credit Private Credit data as of June 2023. Includes upfront fees/OID and assumes average hold of 3 years. Assumptions based on market terms.

Sign up for Blackstone Market Commentary and Pattern Recognition updates.

Opinions expressed reflect the current opinions of Blackstone as of the date of publishing only and are based on Blackstone’s opinions of the then-current market environment, which is subject to change. Certain information contained in the content discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

Certain information and data provided in this content are based on Blackstone proprietary knowledge and data. Portfolio companies may provide proprietary market data to Blackstone, including about local market supply and demand conditions, current market rents and operating expenses, capital expenditures, and valuations for multiple assets. Such proprietary market data is used by Blackstone to evaluate market trends as well as to underwrite potential and existing investments. Additionally, certain information contained in this content has been obtained from portfolio companies and/or sources outside Blackstone, such as press releases, reports, websites, and/or articles, which in certain cases have not been updated through the date hereof. While such information is believed to be reliable for purposes used herein, no representations are made as to the accuracy or completeness thereof and none of Blackstone, its funds, nor any of their affiliates takes any responsibility for, and has not independently verified, any such information. There can be no assurances that any of the trends described herein will continue or will not reverse. Past events and trends do not imply, predict or guarantee, and are not necessarily indicative of, future events or results.

This commentary does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This commentary discusses broad market, industry or sector trends, or other general economic, market or political conditions and has not been provided in a fiduciary capacity under ERISA and should not be construed as research, investment advice, or any investment recommendation. Past performance is not necessarily indicative of future performance.

Joe Zidle

Joe Zidle is a Senior Managing Director and the Chief Investment Strategist in the Private Wealth Solutions group. Previously, he worked at Richard Bernstein Advisors, an independent investment advisor, where he was responsible for portfolio strategy, asset allocation, investment management and marketing to major wealth management firms and independent RIAs. Zidle previously spent nearly a decade at Bank of America Merrill Lynch, most recently serving as Head of Investment Strategy for Global Wealth Management and Deputy Director of the Research Investment Committee, where he was responsible for creating and communicating global investment strategies to the firm’s private client division across all major investment disciplines. Mr. Zidle holds a Bachelor of Arts degree in Economics and History from Emory University. From 1993 to 2001, he served as a specialist in military intelligence for the U.S. Army Reserves.

Jonathan Bock

Jonathan Bock is a Senior Managing Director, co-CEO of the firm’s two business development companies (BDCs), Blackstone Private Credit Fund (BCRED) and Blackstone Secured Lending Fund (BXSL), and Global Head of Market Research for Blackstone Credit.

Prior to joining Blackstone, Mr. Bock was the Chief Executive Officer of Barings BDC. In addition to this role, he served as the Co-Chief Executive Officer and President of Barings Private Credit Corporation, and Chief Financial Officer of Barings Capital Investment Corporation, Barings Corporate Investors, and Barings Participation Investors. Prior to joining Barings in July 2018, Mr. Bock was a Managing Director and Senior Equity Analyst at Wells Fargo Securities specializing in Business Development Companies (BDCs). He was the chief author of a leading BDC quarterly research publication: the BDC Scorecard. He is also published in the Journal of Alternative Investments. Prior to Wells Fargo, Mr. Bock followed the BDC industry at Stifel Nicolaus & Company and A.G. Edwards Inc. Prior to entering sell-side research in 2006, Mr. Bock was an equity portfolio manager/analyst at Busey Wealth Management in Champaign, Illinois.

Mr. Bock holds a BS in Finance from the University of Illinois College of Business and is a member of the CFA Institute.

Stay up-to-date

Email Alerts

To receive email alerts from Blackstone, sign up below.

Portions of this site are directed only to persons in certain jurisdictions. By selecting the relevant option, you certify that it accurately reflects your residency.